Market share and competitive landscape

Within Motoring, the Halfords Group operates in two segments:

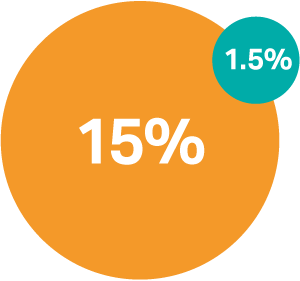

- Car parts, accessories, consumables and technology, with a total market worth up to an estimated £7bn. This element of the Motoring market has grown by around 3% per annum in the last few years. Halfords Retail competes in a portion of this market, holding around a 15% market share.

- Car servicing and aftercare, with a total market worth around £9bn. This element of the market has grown by around 2% per annum in the last few years and is where Autocentres competes, holding around 1.5% share of a highly fragmented market.

There is no single equivalent competitor of Halfords in the UK and these motoring markets are highly fragmented. There are over 30,000 garages in the UK of which two-thirds are estimated to be independents.

Market trends

New car registrations have grown consistently year on year between 2012 and 2016. After a record year for new car registrations in 2016, the Society of Motor Manufacturers and Traders ("SMMT") has forecast a decline in new car registrations of 2.6% in 2017. A reduction in new car registrations typically results in used cars being held onto for a longer time period. Combined with a strong pipeline of cars feeding into the used car category, this means that we anticipate the used car parc to grow in the years ahead. This will be a positive trend for Halfords given that we predominantly support cars that are over three years old, what we call the "second life of the car".

Cars are also becoming more complex and customers increasingly need support for small as well as large maintenance jobs. We are seeing an on going trend from 'do it yourself' to 'do it for me', which plays strongly to our service and services proposition. Our own market research indicates that 80% of Halfords customers want advice or service with their purchase. We also identified that 75% of UK consumers have medium to low expertise in DIY and are therefore more inclined to pay for someone else to "do it for them". We continue to invest in training and equipment to ensure that we remain at the forefront of technological changes, such as having the ability to replace stop-start batteries on-demand and being able to service electric and hybrid vehicles. We estimate that over 50% of the market for car servicing and aftercare is represented by independents, who are finding it increasingly challenging to meet the increasing complexities of cars and their parts.

We continue to see good growth in segments of our in-car technology offering. We are a market leading retailer of in-car cameras ("dash cams") which continued to grow fast in FY17. We are also uniquely placed to offer a fitting service for these products; with around 40% of dash cam sales fitted into the car. Multimedia, connectivity and streaming technology continue to grow as customers look for ways to bring their in-car environment more technologically up-to-date.

The sat nav market continues to decline, but this is becoming an increasingly smaller part of our business, now representing only 3% of Group sales. Across our stores we have an increasing number of accredited child car seat fitters and thousands of colleagues able to fit and provide detailed advice on roof bars and boxes, cycle carriers and number plates. The expert, friendly advice they provide is unique, loved by our customers and key to our further market share gains in these areas.

The services that we offer alongside our products continue to evolve and we now offer a suite of over 30 in-store services for motoring and cycling, complimenting the continued success of our "3Bs" (bulbs, blades, batteries) fitting and cycle repair services.

Going forward we anticipate the Motoring market in which we operate to continue to grow at an average rate of 2-3% per annum over the medium-term and we continue to aim to better those growth rates through our growing service and services proposition.

Halfords Share of the Motoring market

Car parts, accessories, technology, and consumables

Car servicing and aftercare