Opinions and conclusions arising from our audit

1. Our opinion on the financial statements is unmodified

We have audited the financial statements of Halfords Group plc for the period ended 31 March 2017. In our opinion:

- the financial statements give a true and fair view of the state of the Group's and of the parent company's affairs as at 31 March 2017 and of the Group's profit for the period then ended;

- the Group financial statements have been properly prepared in accordance with International Financial Reporting Standards as adopted by the European Union;

- the parent company financial statements have been properly prepared in accordance with UK Accounting Standards, including FRS 101 Reduced Disclosure Framework; and

- the financial statements have been prepared in accordance with the requirements of the Companies Act 2006; and, as regards the Group financial statements, Article 4 of the IAS Regulation.

| Overview | |

|---|

| Materiality: group financial statements as a whole | £3.3m (FY16:£4.0m)

4.7% (FY16: 5.0%) of profit before tax |

| Coverage | 100% (FY16:100%) of profit before tax |

| Risks of material misstatement | | vs FY16 |

| Recurring risks | Carrying amount of

Autocentres Goodwill |  |

| Carrying value of Retail

division inventory |  |

2. Our assessment of risks of material misstatement

In arriving at our audit opinion above on the financial statements, the risks of material misstatement that had the greatest effect on our audit, in decreasing order of audit significance, were as follows:

| The risk | Our response |

|---|

Carrying amount of Autocentres Goodwill (£69.7 million; FY16: £69.7 million) Refer to (Audit Committee Report), (Accounting Policy) and (Financial Disclosures). | Forecast-based valuation Following the acquisition of Nationwide Autocentres in 2010, the Group holds significant goodwill in the Autocentres division. As set out in the Chief Executive's Statement, the results of the Autocentres division were not in line with management's expectations, and, as such, the risk of impairment to the associated goodwill has increased. The business operates in a competitive market, and commercial factors, such as loss of a significant customer, changes to market share or changes to the frequency with which customers replace their cars, may lead to a risk that the business does not meet the growth projections necessary to support the carrying value of the goodwill. The estimated recoverable amount is subjective due to the inherent uncertainty involved in forecasting these cash flows and therefore, this is considered to be one of the key judgemental areas that our audit is concentrated on. | Our procedures included: - Benchmarking assumptions: Comparing the Group's assumptions, in particular those relating to forecast long term growth rates and discount rates, to externally derived data;

- Historical comparisons: Assessing the Group's performance against budget in the current and prior periods to evaluate the historical accuracy of the Group's forecasts;

- Sensitivity analysis: Performing sensitivity analysis on the assumptions noted above, including assumed EBITDA growth of 10% and 0% over the next 5 periods;

- Comparing valuations: Comparing the sum of the discounted cash flows to the Group's market capitalisation to assess the reasonableness of those cash flows; and

- Assessing transparency: Assessing whether the group's disclosures about the sensitivity of the outcome of the impairment assessment to changes in key assumptions reflected the risks inherent in the valuation of goodwill.

|

Carrying value of Retail division inventory (£181.4 million; FY16: £153.3 million) Refer to Audit Committee Report), accounting policy) and (financial disclosures). | Subjective estimate Inventories are carried at the lower of cost and net realisable value. The estimated net realisable value of inventory and associated provisions are subjective due to the inherent uncertainty in predicting consumer demand. Further, changes in the Group's provisioning methodology could lead to inappropriate releases to the income statement. The obsolete stock provision is based on a model which includes consideration of each inventory line, recent sales of those lines and the product's position in its lifecycle. The Group further overlays specific provisions to account for other matters not captured in the model, such as known stock losses and faulty goods. There is a risk that the Group's assessment of the level of these provisions is insufficient or inaccurate. | Our procedures included: - Assessing methodology: Assessing the adequacy of the Group's inventory provision methodology based on our knowledge of the industry and factors specific to the Group.

- Our sector experience: Assessing and challenging the directors assumptions behind the changes to the provision methodology against our own knowledge of the industry and factors specific to the Group;

- Tests of detail: Testing the key inputs to the provisioning model, including recent sales data and inventory costing. Obtaining a report of sales made subsequent to the period end at a negative margin to ascertain whether those items should have been provided for at the period end;

- Historical comparisons: Assessing the accuracy of inventory provisioning by checking the historical accuracy of the level of inventory provisions in prior periods; and

- Assessing transparency: Assessing the adequacy of the Group's disclosures about the degree of estimation involved in arriving at the provision.

|

3. Our application of materiality and an overview of the scope of our audit

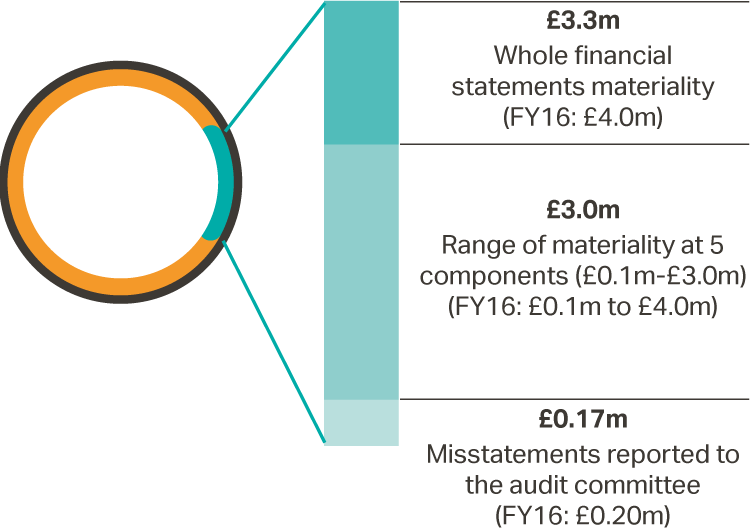

Materiality for the group financial statements as a whole was set at £3.3 million (FY16: £4.0 million), determined with reference to a benchmark of group profit before tax, of which it represents 4.7% (FY16: 5.0%).

We reported to the Audit Committee any corrected or uncorrected identified misstatements exceeding £0.17 million (FY16: £0.20 million), in addition to other identified misstatements that warranted reporting on qualitative grounds.

Of the Group's 5 (FY16: 4) components, we subjected 5 (FY16: 4) to full scope audits for group purposes. All components are located in the UK.

The components within the scope of our work accounted for the percentages illustrated opposite.

The Group team approved the component materialities, which ranged from £0.1 million to £3.0 million (FY16: £0.1 million to £4.0 million), having regard to the mix of size and risk profile of the Group across the components. The work on 5 of the 5 components (FY16: 4 of the 4 components) was performed by the Group team.

Profit before tax

£71.4m (FY16: £79.8m

Materiality

£3.3m (FY16: £4.0m

Profit before tax

Group materiality

Group revenue

Group profit before tax

Group total assets

Full scope for group audit purposes FY17

Full scope for group audit purposes FY16

4. Our opinion on other matters prescribed by the Companies Act 2006 is unmodified

In our opinion:

- the part of the Directors' Remuneration Report to be audited has been properly prepared in accordance with the Companies Act 2006; and

- the information given in the Strategic Report and the Directors' Report for the financial period is consistent with the financial statements.

Based solely on the work required to be undertaken in the course of the audit of the financial statements and from reading the Strategic Report and the Directors' Report:

- we have not identified material misstatements in those reports; and

- in our opinion, those reports have been prepared in accordance with the Companies Act 2006.

5. We have nothing to report on the disclosures of principal risks

Based on the knowledge we acquired during our audit, we have nothing material to add or draw attention to in relation to:

- the Directors' statement of viability, concerning the principal risks, their management, and, based on that, the Directors' assessment and expectations of the Group's continuing in operation over the three periods to 3 April 2020; or

- the disclosures in the financial statements concerning the use of the going concern basis of accounting.

6. We have nothing to report in respect of the matters on which we are required to report by exception

Under ISAs (UK and Ireland) we are required to report to you if, based on the knowledge we acquired during our audit, we have identified other information in the Annual Report that contains a material inconsistency with either that knowledge or the financial statements, a material misstatement of fact, or that is otherwise misleading.

In particular, we are required to report to you if:

- we have identified material inconsistencies between the knowledge we acquired during our audit and the Directors' statement that they consider that the Annual Report and financial statements taken as a whole is fair, balanced and understandable and provides the information necessary for shareholders to assess the Group's position and performance, business model and strategy; or

- the Audit Committee Report does not appropriately address matters communicated by us to the Audit Committee.

Under the Companies Act 2006 we are required to report to you if, in our opinion:

- adequate accounting records have not been kept by the parent company, or returns adequate for our audit have not been received from branches not visited by us; or

- the parent company financial statements and the part of the Directors' remuneration report to be audited are not in agreement with the accounting records and returns; or

- certain disclosures of Directors' remuneration specified by law are not made; or

- we have not received all the information and explanations we require for our audit.

Under the Listing Rules we are required to review:

- the directors' statements, in relation to going concern and longer-term viability; and

- the part of the Corporate Governance Statement relating to the company's compliance with the eleven provisions of the 2014 UK Corporate Governance Code specified for our review.

We have nothing to report in respect of the above responsibilities.

Scope and responsibilities

As explained more fully in the Directors' Responsibilities Statement, the Directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. A description of the scope of an audit of financial statements is provided on the Financial Reporting Council's website at www.frc.org.uk/auditscopeukprivate. This report is made solely to the Company's members as a body and is subject to important explanations and disclaimers regarding our responsibilities, published on our website at www.kpmg.com/uk/auditscopeukco2014a, which are incorporated into this report as if set out in full and should be read to provide an understanding of the purpose of this report, the work we have undertaken and the basis of our opinions.

Peter Meehan (Senior Statutory Auditor)

for and on behalf of KPMG LLP, Statutory Auditor

Chartered Accountants

One Snowhill

Snow Hill Queensway

Birmingham

B4 6GH

24 May 2017